Quarterly Update on GTX, GBFH, FLOW

All are up 20%-50% - here’s why I’m still holding (and maybe buying more)

All companies are up from 20% to 50% from the date of the first analysis. However, I believe there is still a lot of long-term potential for all of them, and some are still worth buying even after the recent gains.

Let’s dive into each of them.

Garrett Motion (GTX) passes through all tariff costs

Here is my original analysis of Garrett Motion and the Q4 update. GTX 0.00%↑

Financials were quite good for the quarter, and they have reiterated their full-year outlook:

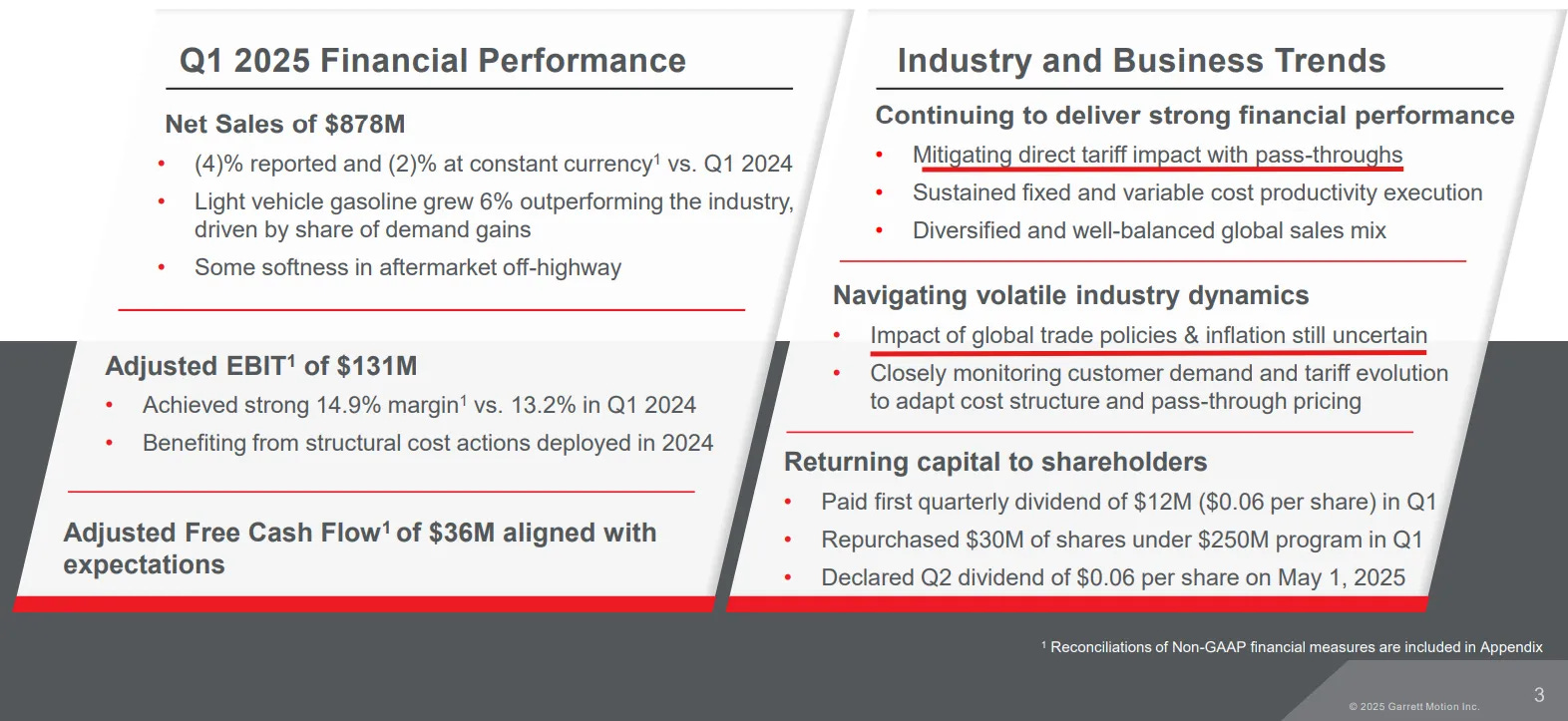

Net Sales stabilized (stayed almost flat YoY) in comparison to previous quarters

Margins (both EBIT and EBITDA) remain very strong, and EBIT/EBITDA are in line with the full-year outlook. Despite weak Net Sales, EBIT has increased by almost 8%, and the margin was 1.7% higher than last year.

FCF looks small, but this is mostly due to expected seasonality in their working capital

Concerning tariffs, GTX was able to pass through all the tariff costs so far. They expect the same for the remainder of the year:

Within the quarter, we delivered $131 million of adjusted EBIT, representing a $10 million increase over the same period last year and a strong margin of 14.9%, up 170 basis points. We achieved this strong performance through $31 million of operating improvement year-over-year, benefiting from price and structural actions taken in 2024 and more than offsetting the impact of lower sales and foreign exchange. In the quarter, we also successfully passed through $4 million or 100% of the impact of newly implemented tariffs, which we expect to continue to do throughout the remainder of the year.

…

We think, and again, we're going to pass them through entirely. If everything stays the way it is today, which is also another if, we think it's around $60-ish million that would be passed through.

Even though they can pass through all the tariff costs, the question is how tariffs will generally impact the industry. If fewer cars are sold, then obviously GTX will be able to sell fewer turbos. For now, the situation remains unclear:

And although we expect to continue to pass through all implemented and featured tariffs, as previously mentioned by Olivier, at this time, there is sufficient uncertainty around the near-term impact new and future tariffs may have on the global economy, which could adversely impact the industry and subsequent demand for turbos. We will continue to monitor these risks and adjust our cost structure to adapt to any changes in customer demand. With that, I will now turn the call back to Olivier for closing remarks.

On the business side, GTX continues to win across all turbo, plug-in hybrids (PHEV), and range-extended electric vehicle (REEV) applications. We see trends reverting from EVs towards PHEVs and REEVs:

We have seen carmakers reviewing their range of products, pivoting to add more hybrids, whether it's North American carmakers or foreign carmakers operating in North America. And with solutions that are, for most of them, implying that they need turbochargers, whether it's plug-in hybrid or something that is growing very much, that's range-extended electric vehicles where the engine provides more of a generator -- electric generator to the powertrain. So we are seeing a strong appeal for that either directly with the carmakers in North America -- the North American carmakers, I should say, or the ones that are operating in North America, meaning foreign brands.

…

we have made significant progress with what I would call the winners in China, some names like BYD, Chery, GD and even new brands that have come like Socon and Seres. Those companies are very innovative, and they are blurring the lines between battery electric vehicles and hybrids by really pushing the development of either plug-in hybrids or range extended electric vehicles and using extensively turbo chargers. So I had really the pleasure to meet with all of these people last week, and they were really reiterating to us that they need our technology moving forward.

They had also made quite substantial progress on the zero-emission technologies side. They won their first major series production award for electric motors, which is expected to start in 2027:

We've reached a significant milestone in the development of our E-Powertrain high-speed technologies, securing our first series production award from HanDe, a leading axle supplier to integrate Garrett's high-speed e-motor and inverter technology into their axle and transmission platforms for heavy-duty commercial vehicle with production targeted for 2027. This achievement demonstrates the substantial potential of our solutions and validates our position, especially in China where battery electric penetration in commercial vehicle tops the rest of the world.

They have refinanced their Term Loan B, and now they don’t have any significant debt maturities until 2032. This gives them additional resilience to navigate future volatility and geopolitical uncertainty.

Since the first deep dive, the position is up already by ~50%. I still feel good about the company and its ability to navigate this uncertain environment, but I don’t want to add more at current prices. I will continue watching and may close a position if it surpasses $15 (unless there are some very positive developments, which will make me hold on to this stock for longer).

As I mentioned in the previous update, I will watch for signs of growth, further debt reduction, and their progress in zero-emission technologies.

GBank (GBFH) was listed on NASDAQ

Original analysis is here, and Q4 update is here. GBFH 0.00%↑

GBank was uplisted to Nasdaq on 2025.04.30 as planned and is now eligible for Russell 2000 inclusion. Inclusion can drive more demand and push the price higher.

Net income was $4.5mln, a 20% increase YoY over $3.7mln last year. But if we excluded the $800 one-time costs for Nasdaq listing, then net income would be $5.3mln, which is actually a 43% growth.

As expected after the last report, they have generated $105mln of credit card transactions in Q1, which is a staggering ~100% QoQ growth. It generated ~$2mln in net interchange fees.

We may see some slowdown in credit card growth in the Q2, since they want to make sure their IT systems and customer service can manage a higher amount of applications, so they are updating and testing them at the moment. I also like that they want to keep all the critical systems inside GBank instead of relying on third parties.

GBank continues to develop and improve its operational credit card systems, including the internal implementation of application landing pages and internal customer service resources. These efforts are a continuation of the Company’s ongoing strategy to ultimately manage all systems directly as opposed to relying on outsourced third parties. Direct control over these critical resources has become more important as we focus are executing on new marketing agreements, create significant additional social media presence, and require related product systems with the ability to perform on a mass scale. Implementation and testing of these initiatives is currently underway with completion anticipated during the third quarter of 2025, which is expected to cause slowing growth in credit card transactions and growth over the short-term. …

And we believe it's going to take about 30 to 60 days to do that. So we may see some slowdown in our growth in our credit cards for the next quarters, but we anticipate that we're going to be able to handle the much, much higher volume of applications. …

So we want to take this little window of opportunity to do that, so to make sure we're ready because we are planning in -- major marketing efforts that are going to be starting in about 60 days -- 30 to 60 days actually, depending on our app. …

So given all that, we think it's going to stay probably flat for a quarter until we start picking up our momentum again into the third quarter.

The slot program (BoltBetz/Konami), which can be a major source of future deposit growth, is finally going to launch in Q2 2025 after the last regulatory approval. It can also boost the growth of the credit card division:

We believe the program is going to launch in this quarter, this second quarter. And like all launches, it will walk before it runs. So I think you'll start to see the deposits increase in the third quarter. And of course, this will be -- the first launch will be with one of the -- with the [ Distill ] as the gaming operator and it's going to be very controlled, but we have some very active players that are going to be participating.

And the beauty of that app is that it's going to use all of our bank platforms. So by that, I mean the pool player accounts, our RTP. And it also, very importantly, is going to, we think, be a very important resource for the credit card because the credit card really fits the pattern of behavior for a slot player where they can load the app with the credit card and participate in their gaming activity.

The core business is also holding up well against falling interest rates, thanks to improved asset sensitivity (as we discussed in the deep dive), loans are performing well, and the pipeline is strong:

As we think about the different components of our top line, specifically net interest income was up $105,000 compared to Q4, mainly due to our growing balance sheet. Year-over-year, net interest income is up approximately $1.1 million or more than 10%, again, on a much larger balance sheet. NIM was down somewhat quarter-over-quarter to 4.47% and there's a good breakdown of that in the release, specifically lower loan yields as the 50 basis points in rate reductions that occurred in Q4 went into effect for our variable rate SBA loans as of January 1. That was offset by lower funding costs and also higher investment yields. Investment yield and investment portfolio is performing nicely with quarterly yield of 4.94%. Overall, we're quite pleased with the NIM and how it's held up. On a bank peer comparison, we expect to remain in the top decile for net interest margin. …

With net at risk nonperforming loans of $5.7 million, that represents only 3.7% of the company's capital plus reserves. So we're very comfortable and pleased with the continued performance of the loan portfolio, and we are encouraged by the fact that specifically, our SBA loan performance continues to outperform our SBA peers. As we think about the future, we're certainly happy to be in a position that we're in with nearly 25% of our loan portfolio being guaranteed by the SBA and USDA. …

And specifically, as we look ahead in SBA and commercial, we still see some positive sentiment really remaining within that group and our customers, specifically, the SBA and commercial pipeline remains quite strong at an expanded pipeline of more than $300 million.

GBank also continues growing:

Total deposit growth of $189.0 million, or 23.4% compared to March 31, 2024.

Total assets were at $1.19 billion, that's up 24% over the prior year. Total loans were at $843 million, which is up 15% year-over-year.

Deposits were at $996 million, so just shy of a $1 billion mark. That's up 6.5% sequentially. Total equity now stands at $147 million for the company. That is up 43% compared to a year ago.

The book value per share also broke the $10 mark and is now at $10.27, that's up by more than 28% compared to March 31, 2024

Gains on SBA loan sales were a bit weaker this quarter:

gain on sale of SBA loans was down approximately $1.5 million compared to Q4 due to both Q4 sales being strong and Q1 being historically a little weaker due to seasonality in the year-end holidays. Year-over-year gain on sale of loans was actually up by $454,000 or an increase of 22%.

At the same time, margins on sales are not growing due to uncertainty around interest rates (currently ~3.8%):

We were hoping that they [margins] start to strengthen. That hasn't happened so far. They kind of remain at where they've been in terms of soft levels. For us, we had forecasted some improvements in the second half of the year. For that to happen, it's -- I think there's going to be a little bit more certainty -- need to be a little bit more certainty on rates and prepayments, which we're not seeing yet. …

But to be clear, we don't expect GAAP gain to return to 10% anytime soon as tying into Ed's comment on our prior conversation. We do think that over time that the GAAP gain for hospitality in particular will get back to a long-term average, which we think is probably close to high 4s and 5% but that might take a little bit of time.

So far, SBA loan origination volumes are good, but sales volumes dropped in comparison to the previous quarter, and margins are suppressed. Let’s see in the next quarters if it’s a temporary effect or not.

I am very pleased with the trajectory of the business. The management delivers on its promises:

They uplisted to NASDAQ

They are launching the BoltBetz/Konami slot machine project in Q2

They have over-delivered on credit card division growth so far

The core business is working well

The price is ~20% up since the deep dive. There is still a lot of potential upside, and I consider it a longer-term holding. That said, it is still very volatile, so I will add more to the position if there is some weakness and it dips below $30.

Flow Traders (FLOW.AS) had another strong quarter

Original analysis is here, and Q4 update is here. $FLOW.AS

FLOW fell down 20% on the earnings report, and now it’s almost where it was before the report. I don’t know why exactly the market freaked out, but here are the possible reasons:

The CEO leaves the company.

I see it as a neutral event for the company. The current CEO was quite new - he has been there only since 2022. I don’t think that the business will be disrupted when he leaves.

The new CEO will likely be Marc Jansen, who has been with the company since 2013 - he started as a trader and went all the way to the Head of Trading.

Unusual new “Impairment of intangible assets” line in P&L

In addition, we recorded a EUR 10.5 million impairment in intangible assets related to some of our digital assets holdings as the value of digital assets experienced pullback in the first quarter after a few quarters of increases. It is important to note that we hedged some of these digital assets holdings, and we saw a corresponding increase in our NTI as an offset in the quarter. However, given IFRS accounting standards have lagged behind the rapid adoption of digital assets, we had to allocate the gains and losses separately above and below the line.

So, this new line is offset by the corresponding amount, which is hidden within the NTI. In the future, we could see an opposite situation, when instead of impairment, we will see a write-up. It is a new type of transaction, which they did not have before, therefore, they did not have this situation before.

15% higher fixed operating expenses

Last year, they started reinvesting all their earnings back into trading capital, so they expect substantial growth. They support this future growth by hiring more subject matter experts and investing more in the technology. The idea is that in the mid- to long-term, topline growth will outpace these increased costs.

I think the entire focus of the firm on really maintaining cost efficiency. Sometimes we highlight the importance of operational leverage in the firm. That is still a top priority for the firm. What I think is a challenge, and that is not just a challenge for Flow as you start investing, as you hire subject matter experts, there is a missing link between the cost and the payout, if you will. So, what we will expect to see is that we have efficiency gains as the company grows. And I think the most important point from an economic point of view, we do believe -- still firmly believe that the top line growth will be higher than the evolution of our cost base, right? So the mid- to long-term perspective is very much on increasing our margins on this front, yes.

The market could have expected higher net income due to the volatility caused by the recent tariff turmoil.

Firstly, volatility was not too high in the first quarter. It was not much different from Q4 2024. All the tariff craziness started in Q2. That’s where we will probably see some increase in earnings. However, we should not yet expect the COVID-level numbers, since volatility levels were still substantially lower than in 2020.

Given the average volatility and headwinds from Other Income and higher fixed costs, we still had a quarter with EPS = 0.84 EUR, which gives us PE = 8 at current prices. And management expects that this situation will occur on a regular basis.

To conclude, as we execute on these 4 key strategic pillars, we are proud to deliver a third consecutive triple-digit NTI quarter, only the second time in our company's history. We are confident that such quarters will be a regular occurrence going forward as we deliver on each of these strategic priorities.

All in all, it’s still my favorite investment idea, given that we get a company which:

has a potential 20% growth rate (ROE of ~20%, while earnings are now fully reinvested back into the trading capital),

trades at a PE ratio of 8,

has almost no debt and market cap, which is not much higher than the trading capital (thus, margin of safety),

and is a natural hedge against the market turmoil.

Flow Traders’ stock is up 30% since the first deep dive. However, I still think it’s a very attractive investment. It’s the biggest position in my portfolio, and I have been adding at different prices ranging from 15 EUR to almost 30 EUR.

The update for ISSC is coming next week, and the new deep dive comes in the next couple of weeks.

Content I enjoyed recently:

Disclaimer:

Maksim Rodin and/or The Double Alpha-Factory own shares of GTX, GBFH, FLOW.AS at the moment of publication.

This article is for educational purposes only. This is not an investment advice. I may buy or sell these securities at any time. Please see full disclaimer here.