Garrett Motion - Cash Flow Machine with 100% Upside Potential

Low risk, high profitability, 20% FCF yield and tremendous buybacks

Executive Summary

20%-30% annual shareholder return in a normal/good case. Or a quick 50%-100% return, if the market revalues Garrett in line with competitors

“High uncertainty, low risk” situation. In the worst-case scenario, GTX will be able to buy back all outstanding shares in the next 5 years and return 10% annually thereafter

Tremendous 20% FCF yield, high profitability, and resilient and flexible cost structure

Catalysts: inclusion back in SP600, “cleaner” capital structure, realization that EV penetration is slower than expected

Most recent update here (May 6, 2025).

Business and History

This is a quick description of GTX’s business from their 2023 10-K:

We provide cutting-edge technology for the mobility and industrial space, including light vehicles, commercial vehicles and industrial applications. Our products include mechanical and electrical products for turbocharging and boosting internal combustion engines, as well as compressing air for fuel cell compressors, and compressing refrigerant for electric cooling compressors. As of 2023, our primary source of sales is associated with the global turbocharger industry for gasoline, diesel and natural gas engines across light vehicle, commercial vehicle and industrial applications. Sales also come from E-Boosting solutions and hydrogen fuel cell compression solutions, already manufactured at scale.

Just for illustration, these are the kinds of vehicles that use their turbochargers:

Their core business is producing turbochargers, which are used in ICEs (internal combustion engines) and in hybrids to improve both performance and energy efficiency at the same time. It’s critical for OEMs (original equipment manufacturers) since turbochargers allow them to meet fuel economy and emission standards without sacrificing performance.

At the same time, producing turbochargers is a highly complex and technological industry. The threat of new entry is low. It is dominated by two main players: Garrett Motion and BorgWarner, who together hold about 65% of the market share globally (with Garrett Motion being number one).

A substantial portion of sales (>80% of OEM sales) is secured already 4 years in advance. It makes it much easier to predict future cash flows.

Some negative sentiment may come from the fact, that they produce turbochargers for the ICE industry, which is expected to be replaced by BEVs (battery electric vehicles). However, turbo technology is much more resilient than ICE industry:

Firstly, turbocharger penetration on ICE-based vehicles is expected to grow in the next years and still be above 50% in 2030.

Secondly, the penetration of turbochargers for hybrid vehicles is higher than for non-hybrid and the share of hybrids will increase. Another plus for GTX is that turbos for hybrids have higher margins.

Lastly, the production of turbocharged commercial vehicles and off-highway equipment engines is increasing. And it’s a very important segment for GTX with ~30% of total sales and higher profitability than their light vehicle business.

They are actively growing their commercial vehicle and industrial applications. In the last quarter, they’ve added marine and back-up power generator projects to their pipeline.

This is what the CEO said about the future of turbo tech:

Here we are talking about turbos for locomotives, big power gen application, big off-highway vehicle application, marine, it's a new territory for us, it's very relevant because it's not only diesel based, we are talking about natural gas, these machines are getting onto the power gen application for data centers.

Facebook and the like want to pay a lot of money to make sure that when there is a power outage, they can spool up their gen set [back-up power generator] at the speed of light, they are ready to pay for technology and this is the technology we bring.

(Investor and Technology day, October 2023)

We are not just pushed out of the market on the turbo side. When you look at -- we gave this forecast by the way, at a time when -- and we've been public about that. We were expecting 41% of battery electric vehicle on light vehicle by 2030. And you know that probably the last trends are probably lower than that.

So the tail that we see on our core business is a long tail, and that tail is fed by a few things.

First, there is a consolidation happening in our industry that goes to the benefit of people that are being the widest portfolio, the most solid position into the industry when it comes to portfolio development but also the financials to ensure that transition.

And at the same time, we're having plug-in hybrids that are coming up, new technologies.

We are talking about that with [ Matt ] a minute ago. And on the commercial vehicle side, we know that the transition will be longer. And on the commercial vehicle side, we learned that with our industrial turbo.*

…

Most of the use of that is for backup power genset for data center, this is booming, and I don't see that slowing down anytime soon.

So our turbo business is extremely resilient long term.

(Q3 2024 Earnings call)

Valuation

The management expects to earn from $1.7 bn to $2.1 bn free cash flow over the next 5 years. And these numbers are not just a random guess. As shown earlier, GTX can see a sizeable portion of their cash flows 4-5 years in advance.

Even if we assume the worst case ($1.7 bn), it means that GTX will be able to buy back all of its shares in the next 5 years. At the moment of writing their market cap equals $1.6-1.7 bn. In other words, it means that GTX has a whopping FCF yield of ~20%. And it is after investing ~$0.5 bn in the new zero-emission technologies.

What is more, this forecast is based on quite a high estimate of BEV penetration of ~41% by 2030. As the CEO mentioned at the Q3 earnings call:

We disclosed a year ago that we are expecting that by 2030, the revenue that we were expecting on the turbo side would be at the same level as 2023. And this was anticipating a BEV percentage that is probably higher than what people have in their latest forecast.

Recently, a lot of evidence has come that the actual penetration slows down. Let’s see what happens in Europe, the US, and China, which account for a majority of Garrett’s sales.

In February 2023, the EU voted to ban all non-BEV cars (including hybrids) by 2035. However the transition does not go as smoothly as expected - EV adoption is slowing down and demand is not strong (Forbes, Motorfinanceonline).

During the recent Paris Motor Show, the BMW CEO raised concerns about the feasibility of this plan. Other manufacturers and some governments agree with him:

BMW CEO Oliver Zipse has called on the European Union to rethink its ambitious plan to phase out petrol and diesel cars by 2035, stating that the target is “no longer realistic.”

The European Automobile Manufacturers Association (ACEA), which represents 15 major automakers, has warned that slower-than-expected EV adoption could lead to "multibillion-euro fines" for companies unable to meet the EU's strict emissions targets.

Italy's Prime Minister, Giorgia Meloni, has described the EU's approach as “self-destructive,” while countries like the Czech Republic, a key automotive manufacturing hub, are calling for greater regulatory flexibility.

EV Magazine: BMW CEO Urges EU to Rethink 2035 Petrol Car Ban Deadline

At the same time, the EU tries to protect its automotive industry against EVs made in China by imposing heavy tariffs (some as high as 45%). EU could have probably imposed a 100% tariff, like the US or Canada, but there is a risk of missing their own 2035 zero emission target.

EV adoption in the US is also not as fast as planned. For example,

The Biden administration on Wednesday slashed its target for U.S. electric vehicle adoption from 67% by 2032 to as little as 35% after industry and autoworker backlash in the political battleground state of Michigan.

Reuters: US eases tailpipe rules, slows EV transition through 2030

From the demand perspective, republicans are still quite reluctant to buy EVs, and the adoption of EVs in republican states is much lower (The Washington Post). If Trump becomes president, it could further slow down the adoption.

McKinsey reported that 46% of EV owners in the US (and 29% globally) would likely switch back to ICE vehicle due to total costs of ownership and too much impact on long-distance trips.

There are also concerns about the profitability of EVs. At the same time, automakers start looking more and more towards hybrids, which offer benefits of both ICEs and EVs while being profitable.

The next generation of Ford EVs will be launched "only when they can be profitable," Marin Gjaja, head of the Model E EV business, told analysts Tuesday.

…

Consumers opted for hybrid vehicles and family SUVs instead of EVs for convenience and relative ease in terms of maintenance.

In response, Ford and GM, which were putting together ambitious EV plans, have begun leaning toward their higher-margin hybrid and gas-powered models.

Reuters: Ford slows EVs, sends a truckload of cash to investors

Same in China:

Several Chinese carmakers that used to exclusively offer battery-electric vehicles have announced plans to start making plug-in hybrids or range-extended electric vehicles, both of which rely on engines along with onboard batteries.

…

”The pure electric-vehicle firms are not profitable,” a senior Geely [Chinese carmaker] executive said.

With the sole exception of Tesla, no pure EV producer has managed to get out of the red. Chinese companies BYD and Li Auto are profitable, but they also make plug-in hybrids or focus on extended-range EVs.

Bloomberg: China’s EV Makers Turn to Hybrids in Pursuit of Elusive Profits

In my opinion, it’s becoming more and more evident, that transition to BEVs will not be as smooth and as quick as politicians and climate activists want.

It gives me the confidence, that at least the GTX’s worst cash flow forecast ($1.7 bn over 5 years) will materialize, which means that they will be able to buy back all their outstanding shares in the next 5 years or 20% FCF yield.

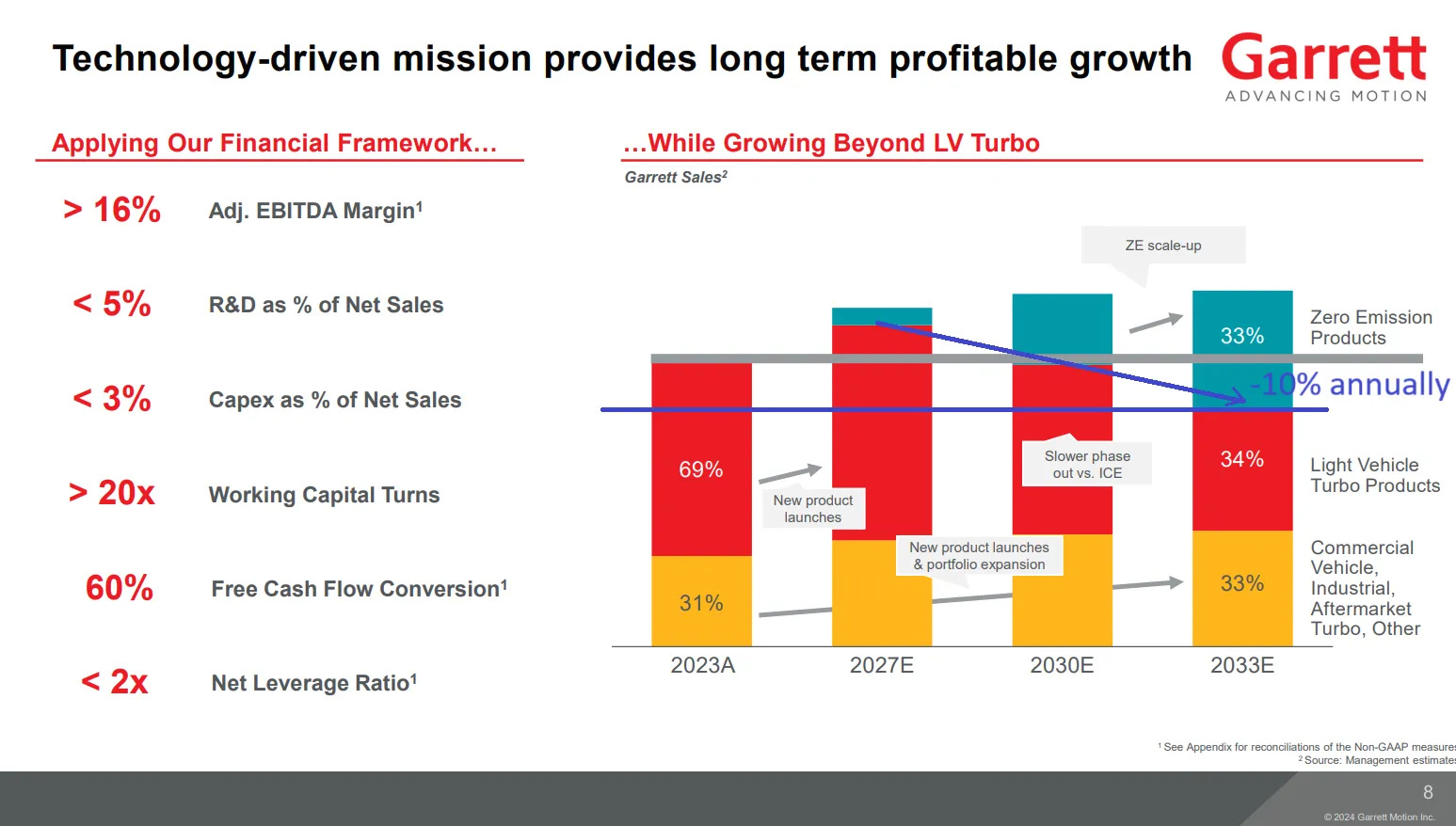

Also, it’s not that they suddenly stop making any profits on turbo after 5 years. The turbo production for light vehicles will just slowly decrease over time. After that, GTX will still have revenues from their CIA business line (Commercial Vehicle, Industrial, and Aftermarket).

If we look at their recent (August 2024) revenue projections, we can roughly estimate that they expect turbo business to decline ~10% annually. Even if we assume zero revenues/profits from their Zero Emission products, we can still expect 20% (current FCF yield) - 10% (decline rate) = 10% return on investment after the next 5 years.

So, my worst-worst case scenario gives me 20% returns in the next 5 years and 10% returns thereafter. I consider this a high enough margin of safety.

From the relative valuation perspective, Garrett’s closest competitor BorgWarner (the second in the turbo duopoly) is traded at FCF yields of ~8-10%, which is twice lower than Garrett’s. It means a potential 50-100% upside for GTX if the market revalues it in line with the competitor.

“Free” option on the success of their EV technology

The valuation exercise we performed above was only about their turbo business. At the moment, Garrett is actively investing in their Zero-Emission (ZE) technologies, which include Fuel Cell Compressor, E-Powertrain and E-Cooling Compressor.

They believe that they can combine their deep technological knowledge in the turbo industry (which is highly relevant to the new technologies they invest in) and their strong and collaborative relationships with leading OEMs to successfully bring their Zero-Emission products to the market and deliver $1 bn annual Zero-Emission sales by 2030 (vs current $3.5-4 bn).

GTX has already won a lot of contracts:

11 series production contracts for their Fuel Cell Compressor (up from 5 a year ago)

15 pre-development contracts for their E-Cooling and E-Powertrain solutions (up from 5 a year ago)

In 10 years, GTX expects to have ~1/3 of sales in each of the three segments: Zero Emission Products, Light Vehicle Turbo, and CIA Turbo. It’s important to note here, that the profitability of both Zero Emissions and CIA is higher than of Light Vehicle, which may secure Net Income and FCF growth even if sales are less than planned.

Now, even if they are not very successful in growing the ZE segment, it could still partially offset the decline in turbo. Let’s say, they manage to at least cover the decline in turbo, which means a 0% growth rate. Then we already have a 20%-return investment (just the current FCF yield).

The point here is that if the ZE segment proves to be successful, the stock has a potential for 25%-30% annual returns (20% FCF yield + 5-10% growth from ZE).

“Messy” history but stellar capital allocation

Garrett has a “messy” history and that could be one of the reasons, why it is still undervalued.

The company was spun off from Honeywell (which is a multinational conglomerate) in 2018. During the spin-off, GTX got an asbestos liability from Honeywell, which was completely unrelated to the business of GTX. They could not pay it back and filed for bankruptcy in 2020.

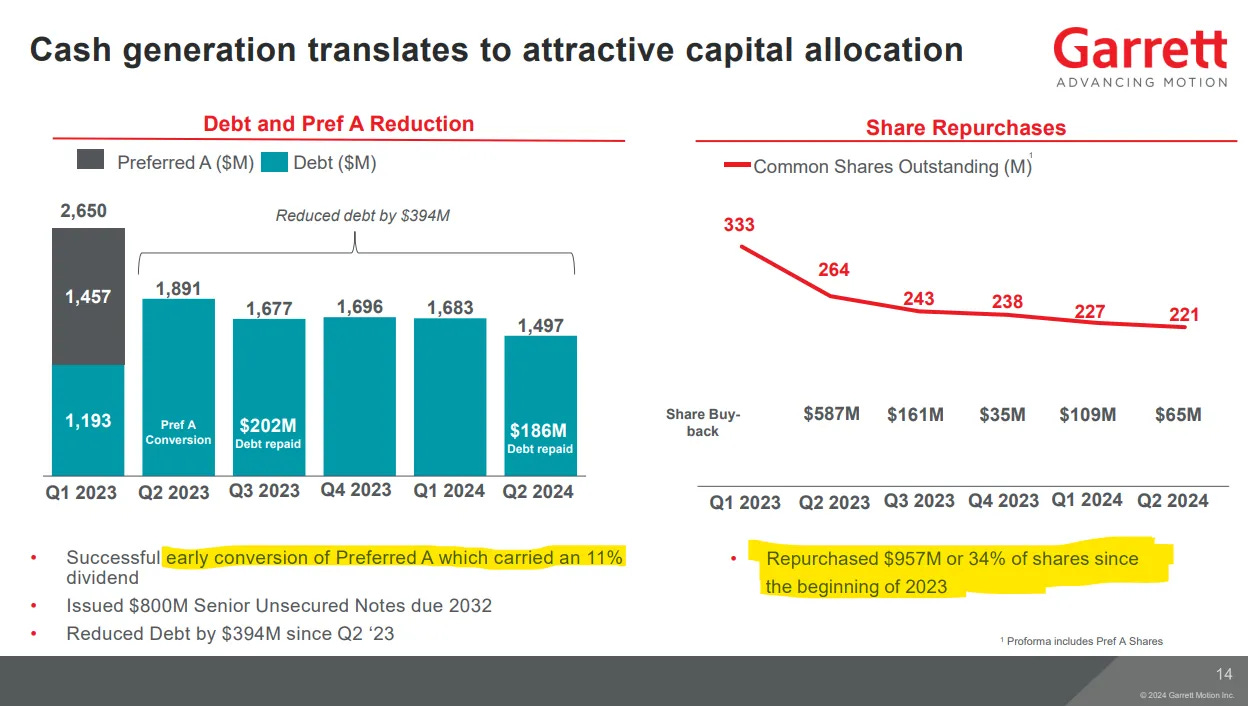

After the bankruptcy, Garrett had a complicated capital structure, which included a lot of preferred shares. In 2023, Garrett finally got rid of the preferred shares - they have partially repurchased them and partially converted them to common stock. They’ve used additional debt for this purpose, but it had a much lower cost.

The slide above perfectly illustrates this process. So, during the last 1.5 years, GTX:

Got rid of very costly preferred shares, which carried an 11% dividend,

Paid back ~$400 mln debt,

And at the same time managed to buy back ~20% of common shares (in addition to the $570 mln repurchase of the preferred shares)

This says a lot about the ability of GTX to generate Free Cash Flows and allocate it in a shareholder-friendly way.

At the moment, they are actively working on reducing their debt. In Q2 2024, both S&P and Moody's increased their ratings to BB+ and Ba1 respectively (this is one level away from investment grade rating). In Q3 2024, Fitch upgraded the outlook of their BB- rating to positive (meaning that it will most probably improve in the next few quarters).

To get to the investment grade, GTX will probably have to bring its net leverage ratio down to 1.5-1.8x, which is an average value for companies with lower-level investment grades. Their competitor BorgWarner has a ratio of ~1.5x and an investment grade rating of BBB+ (according to Fitch).

For that, GTX will need to pay back another $300-500 mln, which represents ~20-33% of their current debt. Their current interest expenses are ~$150 mln, which means GTX can reduce its interest expenses and increase its annual cash flows by ~$30-50 mln (150 * 20% and 150 * 33% respectively). It will probably be even more since they will be able to secure better interest rates with higher grade.

A lot of institutional investors

During the bankruptcy process, this stock attracted a lot of attention from various distressed debt, private equity, and value hedge funds. The main risk here is that we don’t know when these funds sell. And their selling can create a downward pressure on the stock price.

Oaktree and Centerbridge massively supported Garrett after the bankruptcy. They held a lot of preferred shares. After their conversion to common stock in April 2023, they contractually agreed not to sell any shares till November 27, 2023. After that date, they could sell up to 50% of their holdings. They will be free to sell 100% after November 27, 2024.

Despite this, Oaktree has not sold any of its 44 mln shares. Centerbridge has sold ~10% (down to ~38 mln from ~42.3 mln after conversion), slower than the buyback rate. I would argue, that if they did not see any potential (probably another 50-100% up), they could offload their stock much sooner.

For example, famous deep value / special situation investor Seth Klarman with his Baupost Group sold all their ~30 mln shares over a few quarters after the conversion. Sessa Capital has already sold almost 50% of its original stake. Cyrus Capital has sold ~20% since 2023.

There are also some funds that have been cumulating the position in Garrett. For example, Hawk Ridge has increased their stake by ~30% since 2023, while William Blair Investment Management started buying only in 2024.

In my opinion, the risk that Oaktree and Centerbridge decide to quickly exit their positions is rather low. And even if they do, massive buybacks will make sure that the pressure on the price is not too high.

Resilient and flexible cost structure

The last point I want to mention is their resilient and flexible cost structure. This year was quite tough due to softness in Europe and China and general industry weakness. Sales were 14% down in Q3 2024 in comparison to Q3 2023. But what is fascinating is that margins got stronger (improved by 1.6% to 17.4%) and EBITDA was almost the same (FCF even higher).

This is how the CEO explains it in the Q3 2024 earnings call:

So today, it's the result not only of 1 quarter of effort, we've been working diligently for the last 2 years even more on that because we were seeing -- we were anticipating that there could be some softness. We had identified pockets of inefficiencies, and we are always working on these things.

So it's not like a 1 quarter effort. We work at making our factories more flexible. We work at decreasing our fixed costs into the factories as an example. And we had a big plan going on for the last year on these things.

So there is, obviously, as we got on deflation on some specific raw materials, the impact of that deflation into the improvement of these margins, and that could fluctuate obviously, on that. But most of the effort is coming from, I should not say, hard [ core ] costing measures, but adapting the structure, working on efficiency, developing new systems, new processes and everything across the company.

They had also a similar situation during COVID. So, the business of GTX is much stronger and less cyclical than the automotive industry in general.

Their margins are also best in class across the industry:

Conclusion and why the opportunity exists?

I see a few reasons, why this opportunity exists:

Recent “messy” history including bankruptcy made it harder to “screen” for normal investors. As time passes, more investors will appreciate tremendous FCF yields, high profitability, and resilient and flexible cost structure (much better than average in the automotive industry).

Garrett Motion was kicked out of the SP600 index in 2020 when it went through the bankruptcy process. Now, there is a high probability that they will return to the index. This will make GTX more visible to retail investors and trigger purchases from ETFs exposed to SP600.

There is too much unfounded optimism about the EV market. I believe, that it will become more evident for a majority of investors in the next 1-2 years.

In my opinion, this is a “High uncertainty, low risk” situation, which Mr. Market normally hates.

There are a lot of unknown variables: what will be the rate of BEV penetration, how successful will be the new Zero Emission segment, how many new turbo industrial projects GTX will win, and so on.

At the same time, the risk of losing much on this investment is low, since the company will generate tons of cash even in the worst-case scenario. It will be enough to buy back all outstanding shares in the next 5 years and return 10% annually thereafter.

On the other hand, the upside in a normal/good case is quite significant - we are talking about 20%-30% annual shareholder return, depending on the case. Or a quick 50%-100% return, if the market revalues Garrett in line with competitors.

Further reading on Garrett and the EV market

If you are interested in diving deeper into the history of Garrett Motion, I encourage you to read a great series of posts by Six Bravo. Links to other posts are inside this one:

If you are interested in reading more on the EV market and platinum, read this recent analysis by Trader Ferg. The analysis part is free and I enjoyed it a lot. I’ve used a few links from it as well.

Disclaimer:

Maksim Rodin and/or The Double Alpha-Factory own shares of GTX at the moment of publication.

This article is for educational purposes only. This is not an investment advice. I may buy or sell these securities at any time. Please see the full disclaimer here.

Hi Maksim,

Thanks for the write-up. Interesting opportunity.

The share buybacks make sense with this share price. However, one of the risks might be that the FCF deteriorates, which would bring the consequence that more of the FCF would be needed to reduce the debt on the balance sheet in order to keep the EBITDA relative to the debt within appropriate boundaries. This would obviously impact the ability to repurchase shares, which is one of the key drivers in the returns here it seems.

From a FCF deterioration perspective, the revenue seems to be in a increasingly negative trend looking at the revenues on a quarter by quarter basis for the at least the last four quarters. The problem seems to be within Gasoline and Diesel and the lightweight vehicle sales. In addition, it also looks like that management is not really having grip on it, as they are lowering their revenue outlook quarter over quarter – note they started with 0% growth expectation in the beginning of this year, which they reaffirmed following the Q1 figures, while they are currently – disclosed in the Q3 earnings call – are expecting a 11% decrease. It seems that either management is not really in control or that this business maybe is not as predictable as they are trying us to believe. What evidence do you have that revenues will not further decrease?

Finally, they mention that OEM sales is predictable with ~80% being contracted several years in advance. Do you know how they define OEM sales? What is the percentage of OEM sales in total revenues? I wasn’t able to quickly catch this from their disclosures.

Best regards,

Harrie

There is one big caveat to this thesis. For the record, I've followed GTX closely since spinoff in 2018, having done extensive research, and I am still invested with a small position that I'm likely selling within a few of months.

The thing is, the world of auto manufacturing is being somewhat disrupted on a macro level by the raise of China, out of nowhere, as the world's largest producer and exporter of cars. Also, there's a price war in China and competition between brands is extreme. I think all this puts extreme presure on Western OEMs going fwd (I believe we'll see OEMs going bust yet again in the coming years), and they are GTX's main customers. The company has acknowledged this in their last couple of quarterly calls, as well as the fact that they are aware of their IP having been copied by local manufacturers in China, where they have less patent protection resources.

All in all, I think this is a well run company implementing excellent capital allocation policies, but whose (formerly excellent) business is fundamentally impaired going forward. Hence I see fwd returns as 20% from capital allocation, minus some significant % coming from recurring revenue losses (~10% YoY in the last 2 quarters), call it ~10-15% prospective return altogether, not worth the uncertainty in my view, especially for a cyclical industry like autoparts; remember that 80% contracted revenue is contingent on volume sales, so if less customer OEM cars are sold, that revenue will be proportionately lower. I give 0 value to zero-emission tech that probably won't ever amount to much vs their turbo business given the low adoption of BEV mentioned in the article; I actually tend to see those $500M of R&D for zero-emission products as potentially wasted, if we continue down the current path regarding BEV adoption; maybe just an expensive PR exercise targeted at ESG-minded institutional investors when it's all said and done.

Just my 2c.

Regards