Flow Traders - antifragile company with potential 50% earnings yield

High ROC, no debt, priced as if there will never be any market turmoil

Executive Summary

“High uncertainty, low risk” investment and a hedge against market volatility/turmoil - company generates abnormal profits when market volatility and trading volumes increase

At the same time built to survive even during low volatility environments - never had an unprofitable year, FCF conversion averages 90%

High returns on trading capital of 50%+ (up to 100%+ during higher volatility times) and prudent capital allocation

Almost no debt now, but slowly starting to use this opportunity to leverage their high returns

Employees with “skin in the game”

Priced as if there will never be any market turmoil in the future

Most recent update here (May 6, 2025).

Liquidity provider specialized in ETPs

I first stumbled upon this company 2 years ago and have been following it ever since.

Flow Traders (FLOW) is a global multi-asset liquidity provider. They use their proprietary technology to quote both bid and ask prices in various financial assets (both on- and off-exchange) and make money from small price differences between buying and selling related or correlated assets. As an Authorized Participant (AP) they also participate in creation and redemption of ETPs.

In other words, when you buy or sell your ETFs, it is often Flow Traders who is your counterparty in the transaction. They make the market more liquid, efficient and reduce bid-ask spread.

FLOW does not have any Assets under Management (AuM), nor does it sell any products or services to any customers. They use only their own capital and their value chain comprises of institutional counterparties, prime brokers and regulators.

Flow Traders has started as a specialist in equity ETPs in EMEA region in 2004. Since then they became the leading ETP provider in EMEA region with ~30-40% market share (one of the two dominant players, another one being privately held Jane Street). They have access to more than 180 trading venues and exchanges (Nasdaq, Xetra, LSE among others) in 40 countries and to more than 2400 institutional counterparties (banks, pension and hedge funds, insurance companies, etc.). They have expanded their expertise into other regions (America and Asia) and product types:

equity index products

single bonds and bonds ETPs

futures, spot and ETPs for commodities, crypto and currencies

Additional optionality from venture capital and digital assets

In 2022 they also launched their corporate VC to invest (normally as a minority investor) into companies, which are focused on building market infrastructure, connectivity and data solutions (mostly in digital assets field). The main point here is that they are searching for companies, which are closely aligned to FLOW’s core business and commercial agenda and can be integrated into their existing platform or where their platform can be leveraged.

This is a long-term project and is limited to €50mln stretched over 2+ years, which is not too little but also not too much for FLOW. Venture cap investments are obviously risky, but there is a potential for outsized returns and a greater scale in long-term. I mainly consider it as an option on the future wider adoption and use of digital assets and blockchain by larger institutions.

This is what CEO said about their strategy concerning crypto and blockchain (from Capital Markets Update 2022):

There is a conviction that efficiency and effectiveness of blockchain technology, the opportunity of markets becoming totally interoperable, fully connected - is an opportunity in itself we [Flow Traders] cannot ignore. And I would even make that statement on top of Flow Traders - the financial community cannot ignore that opportunity.

It is also defensive play - if you allow a thought for a second that maybe in 5-10 years a significant portion of global liquidity is in tokenized asset platforms, then a market maker could take a very interesting and important place in it, in driving this evolution and enabling it, delivering use cases to attract institutional appetite and create stability in this evolution

I agree with these statements and agree that blockchain technology will most probably be more and more important in our life and, in particular, in finance/trading. This is exactly the kind of exposure to crypto I would like to have - not via direct investments in digital assets, but via investments in underlying infrastructure and collecting fees from others trading these digital assets.

In this regard, FLOW qualifies as both adjacent (constantly adding new product types) and embryonic (corporate VC) spawner in Monish Pabrai’s spawner framework to identify 10-100x baggers.

A few secular trends will help to grow

There are a few interconnected trends, which may help FLOW to grow further:

ETP market has been growing rapidly in the last years and there is still a lot of room for growth (from $8 trillion in 2020 to $12 trillion in 1H 2024 to expected $25 trillion in 2030)

The electronification of fixed income trading (and other assets) is accelerating in the last years

Crypto market and blockchain technology is getting traction and more attention from larger institutions (e.g. recent launch of Bitcoin ETFs in U.S. or Bitcoin futures on Eurex)

Number of regulations is growing and according to CEO: “Regulation for us is a big plus” . FLOW has been regulated since the beginning and has built strong relationships with regulators and can accelerate the regulatory dialog to drive growth (in particular, around digital assets).

Employees with “skin in the game”

FLOW emphasizes its remuneration policy a lot. They try to align interests of all employees - not only Executive Directors - with the interests of shareholders. They share one singular firm-wide variable remuneration pool (for all employees and Executive Directors), which is equal to 32.5% of operating profit. Then every employee is entitled to receive variable remuneration relative to their contribution. Each individual Executive Director’s compensation is capped at 20 times the average FTE (full time equivalent) total remuneration.

To stimulate risk awareness a significant part of any profit sharing (62.5%) is deferred for a multi-year period (up to 4 years). This part remains fully at risk, since these outstanding deferrals can be reclaimed back if company suffers losses in one of the next years.

In good financial years, the pay-mix is skewed towards variable remuneration. Apart from that, almost every employee is an equity holder, since quite a substantial part of variable compensation is paid in shares.

I like this strategy, since it’s focused on hiring and retaining the top talent as well on aligning their interests with those of shareholders. Also, this reminds me a bit of “economies of scale shared” concept of Nick Sleep - all stakeholders win:

Employees share profits and, therefore, work more effectively and efficiently

The more efficient FLOW’s algorithms work, the better prices their customers have and the happier they are

The happier they are, the more business grows

Abnormal profits during market turmoil

The interesting pattern in the financial performance of FLOW as a liquidity provider is that they generate abnormally high profits during the periods of higher volatility (and more trading volume) in the markets. At the same time, they have never had a negative FCF or Net Income year even during the lowest volatility times. FCF conversion averaged ~90% in the last 10 years.

On the slide below it is seen, that higher volatility levels generally produce higher margins and Net Trading Incomes (or NTI, which is gross trading income minus direct costs, like trading fees, financing and hedging costs), though it’s not a perfect correlation. CEO also mentions that the more diversified their trading strategies become, the bigger these peaks of outperformance will be in the future, which is exactly what they mean by improving structurally (more about it in a moment).

The slide above does not include latest NTIs, which were €481mln for 2022, €297mln for 2023 and €206mln for H1 2024. Volatility was quite subdued in 2023 and H1 2024, therefore NTI in 2023 was not very impressive. The main reason, why H1 2024 was so good despite lower market volatility, is that FLOW capitalized very well on the launch of Bitcoin ETFs in Q1 2024. It shows how quickly and effectively they can move capital between asset classes and different trading opportunities.

There was an increase in market volatility in the beginning of August 2024 (with intraday VIX rising to 60 points), and it’s interesting how much FLOW managed to capitalize on this opportunity. Final numbers for Q3 are not published yet, but from the recent Q3 pre-close call we can see that it did have a positive impact on NTI across all asset classes. I will definitely check this, when Q3 results are out.

Management is focused on long-term structural growth of Net Trading Income instead of pursuing shorter-term higher-risk opportunities. Four points, which they constantly focus on are:

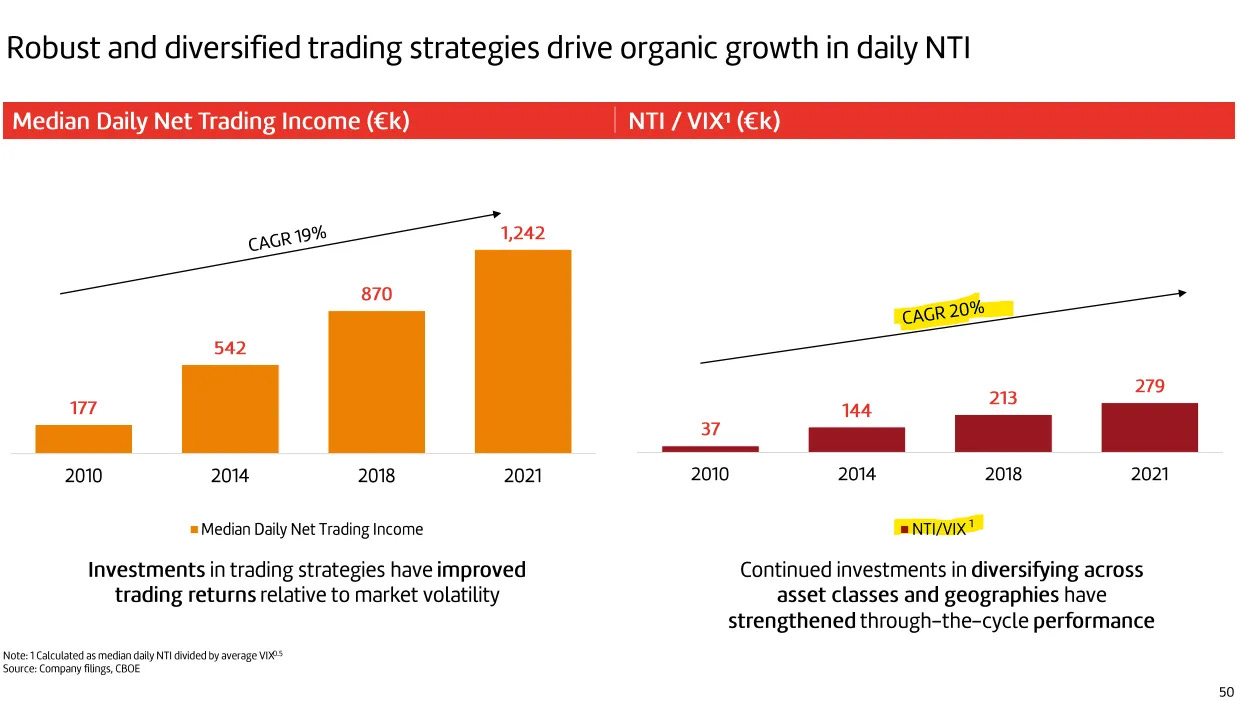

1 — Strong and consistent through-the-cycle financial performance. They are constantly adding more robust and diversified trading strategies to improve returns on capital irrespective of market volatility. One of the three main KPIs they use (apart from EBITDA margin and ROE) is median daily NTI normalized for volatility.

2 — Healthy EBITDA margins. Costs control and maintaining margins is a big part of the strategy.

3 — Maintaining desired risk and resiliency level, so that to be profitable and survive during any market environment

4 — Positioning themselves in such a way, so that to outperform during high volume / high volatility times (velocity of capital)

High ROC and prudent capital allocation

One of the most important measures for FLOW is Trading Capital and return on it. Trading Capital is equal to their net position (all long positions minus all short positions at prime brokers/clearings) plus cash & cash equivalents. They calculate returns on Trading Capital based on NTI - not on Net Income (for reference, Net Income is on average ~30-40% of NTI) - but these returns are still staggering. You can see again on the slide below that returns are much better during higher-volatility times (especially 2020), but are still very strong even during lower-volatility periods.

Another point, which is important for me, is how clean their balance sheet is. They have no goodwill, no intangibles and almost no debt. They have only €30 mln worth of CVC investments. It means, that their Trading Capital is fully financed by their equity. Trading Capital is normally slightly higher than equity, because they use deferred variable compensation (and some other liabilities) as an additional source of capital.

Apart from that, they are very well covered from the regulatory perspective - they have ~€200 mln of excess capital (after redomiciling they have even more).

FLOW’s current market cap (which fluctuated from €800 to €900mln during writing) is only slightly higher than their Trading Capital (€624mln). And it was equal to Trading Capital just two months ago, meaning that the whole company (including its platform, infrastructure, employees, connections with regulators, etc.) was valued at €0. This creates an additional margin of safety. Of course, it’s not really cash and they need it for business, but it’s still a very liquid asset.

Another important point is how they recently changed their capital allocation framework. As they presented it on Capital Markets Update in July 2022, they had four pillars:

Invest

Invest in long-term organic growth of trading capital base while controlling for operating expenses.

Return

Since many years they’ve been paying out minimum 50% of net profit as a dividend. In 2020, they actually paid out €6.5 per share, which is ~30% dividend yield at a current price of €20, and bought back ~3.5% shares back.

Acquire

This is about their Corporate Venture Capital unit we discussed above.

Leverage

Back then in 2022 the CFO (who is now CEO) mentioned that leverage was still an active item on their agenda, and that they started thinking about optimizing balance sheet to further build the trading capital base. Which makes sense, taking into account how high the return on their trading capital is.

Fast forward to Q2 2024, they have announced a “Trading Capital Expansion Plan”:

So, what is my take on this? Firstly, management decided to grow faster only when they were confident that they can sustain this growth. In the previous years, they had been telling that they were slowly building their capabilities, so that in the future they could have more opportunities to deploy their trading capital. And now, when they’ve built these capabilities, they can allow to accelerate the growth.

Secondly, management could have kept the dividend and just taken additional debt. It would be less painful for the short-term stock price, which fell down 20% on the announcement of the dividend cut. Instead, they did what is much better for the long-term but a bit painful for the short-term - namely, they decided to use their retained earnings for growth.

Thirdly, it also makes a lot of sense to take a bit of debt. The CEO mentioned in the earnings call that the cost of debt is less than 10% and they expect it to reduce as they scale up. Compare this cost with 50%+ (and sometimes 80%-100%+) returns on their trading capital. Plus, they say that they are going to be really conservative with it and plan to have it maximum up to 50% of the trading capital (in line with industry).

Founders still retain a sizeable stake

Flow Traders was founded by Roger Hodenius and Jan van Kuijk, who left Optiver - another proprietary liquidity provider from the Netherlands founded in 1986. They were both co-CEOs until 2014 (shortly before IPO) and then continued as Non-Executive Directors of the board. Roger Hodenius has left the board in 2023, while Jan van Kuijk was just re-elected for another 4-year term and continues to serve as a Vice-Chairman.

They still own about 23% of stock together. There is always a risk, that one or both of them will sell their stock and temporarily put the price under the pressure. After IPO they had ~28% and sold 5% in the period before 2018, but they haven’t sold any more shares since then. So, I don’t think we have a big risk here. Also, they both hold a specific right to nominate one Non-Executive Director for election and replacement while they hold more than 5% each.

Surely, I would prefer founders (especially who own substantial amount of stock) to continue to manage the company. On the other hand, there is an evidence now that the company could grow and move forward even without an active involvement of the founders since its IPO.

A management has changed recently - current CEO was appointed in the beginning of 2023. He joined the company a bit earlier in 2021 as a CFO. The previous CEO has led the company since the IPO. But as I pointed out above, I am satisfied with the recent actions of the current management.

Competition

The closest publicly traded competitor is Virtu Financial (VIRT). They are a few times bigger and they also provide some other services to their clients, but still derive most revenues from market making. There are a few points I did not like about Virtu.

Balance sheet is not as strong. Their equity consists mostly of goodwill and intangibles (and a bit PPE) and all trading capital (~$1.8 bln) is, therefore, financed by long-term debt (~$1.7 bln). They made a few big acquisitions in the past and financed them with quite a lot of debt. Ratios as of the end of 2023 are: Debt/Equity = 1.21 and EBIT/Interest = ~4. Also, Virtu’s fixed expenses are higher, while net margins and ROE are lower.

In contrast, FLOW has just started issuing debt and has quite a long way to go. Moreover, they are more conservative with it (at least for now) and don’t plan to have more than 50% of trading capital as debt.

Priced as if there will never be any market turmoil

The company itself aims to grow NTI at ~20% CAGR, which is a very ambitious target (though they managed to do it historically). I would use a conservative estimate of 5% for the organic growth. I expect that they will make around €1-2 EPS in a low volatility environment (based on their performance in such periods in history), which corresponds to 5%-10% earnings yield with a current price of €20 (compounded as retained earnings, which will be even better with P/B > 1). This gives me a total return of 10%-15% in a worst case scenario - low growth and low volatility forever. Some market turmoil and higher volatility can easily shift these returns into 20%+ zone.

However, if there is a crash, FLOW can do 50%-100% in one year, as already happened during the COVID. Back then they made €465mln in Net Profit, which is more than 50% of current market cap. Management constantly emphasizes the fact, that they are even more ready now to take advantage of any extreme events.

I see margin of safety in a few things here:

FLOW’s trading capital (and book value) almost equals their market cap (~70-80% of it at the moment)

FLOW is like a hedge against market turmoil/crash for the portfolio

FLOW has almost no debt

In my opinion, FLOW is priced now as if there will never be any volatility spikes or market turmoil in the future and the company will have a very small organic growth.

Why does the opportunity exist?

I see a few reasons, why this opportunity exists:

This situation is what Monish Pabrai calls “High uncertainty, low risk” - cash flows can vary a lot from year to year, since they depend a lot on volatility, but they are always positive and are structurally growing, so there is low risk. And Mr. Market hates uncertainty and rarely looks beyond the next few quarters. Every time I check their earnings call, there are a few analysts, which are unhappy because they cannot predict and model FLOW’s future earnings.

This is quite a small Dutch company and is not so liquid, so big sellers can press the price down. You could see the example of this, when the company dropped 25% in a couple of days when they announced their “Trading Capital Expansion plan” (which included the dividend cut) in the 2024 Q2 earnings call.

Flow is not screen-friendly. It looks like they have a lot of assets, liabilities, cash and debt, while these are just their long and short positions.

Risks

There are a few risks to take into account before investing:

From my perspective, the biggest risk is technological. FLOW’s main competitive advantage is their proprietary platform for trading, and it’s impossible to understand how exactly it works and whether it can really perfectly (or almost perfectly) hedge any exposure. However, they managed to have no losses until now and they have implemented a senseful remuneration philosophy, which stimulates risk awareness not only among managers, but also among employees.

Management is quite fresh - current CEO serves from the beginning of 2023 (he also served as a CFO from 2021) - and one co-founder has left the board. On the other hand, my impression from listening to the earnings calls and other presentations is that management really puts long-term goals and long-term value creation on the first place, which is good for long-term investors. They think about sustainable long-term growth of trading capital and earnings and prudent/rational capital allocation instead of paying too much attention to what analysts want from them.

Trends, which we discussed above, may not materialize. If they don’t, then there is less organic growth for Flow Traders, but then there is probably more turmoil in the markets, which will help in the short-term. Vice versa, if we have low volatility forever, then financial markets will probably grow fairly steadily, which will boost the organic growth.

There is always competition, and it’s not that they have an unbreachable moat. But they constantly navigate their environment, they have strong connections with regulators, they constantly add to their pool of trading strategies, and they search for and invest in the new opportunities and the ecosystem development.

Content I enjoyed recently

I borrowed this idea of sharing the content from

. I hope they don’t mind.

Disclaimer:

Maksim Rodin and/or The Double Alpha-Factory own shares of FLOW at the moment of publication.

This article is for educational purposes only. This is not an investment advice. I may buy or sell these securities at any time. Please see full disclaimer here.

What a great quality write up. I have been invested in Flow Traders for 3 years now and I have to say you are on point.