ISSC: A Hidden Gem in Aerospace Poised for Explosive Growth or Acquisition

Shareholder/management activity, reduced selling pressure, recent strategic acquisitions and growth projects, and temporarily depressed margins create a great opportunity to buy

Innovative Solutions & Support, Inc. (ISSC) is a misunderstood micro-cap aerospace company that has quietly repositioned itself from a volatile aftermarket provider into a stable, predictable OEM player.

There is now an opportunity to buy ISSC, as its price dropped by 40%+ following the quarterly earnings miss combined with a general market pullback (even though this quarterly report showed good developments) - below the recently offered acquisition price.

Most recent update here (May 15, 2025).

Attractive Acquisition Target

Nine months ago, in May 2024, Christopher Harborne, ISSC's biggest shareholder (with a 15% stake at the time), offered to buy the whole company for $7.25, 5% more than today’s price. The board rejected this offer.

Another interesting fact is that recently both the CEO and freshly hired CFO amended their employment contracts to add significant financial protection for themselves in case of a Change of Control event (a.k.a. acquisition):

The CFO, who was hired only in March 2024, amended the contract on 12.06.2024

The CEO owns quite a lot of equity - roughly 5% of outstanding stock (from the latest definitive proxy):

~300k stocks and soon-to-be-vested RSUs

~250k exercisable options (at $8.1 exercise price)

~100k unexercisable options (also at $8.1) and unvested RSUs

In addition, a couple of months ago, he was given 200k PSUs with Vesting Prices of $10, $12, and $14.

And last, but not least, management seems to pay taxes on RSUs from their own pockets. From the Q2 2024 call (at the time when the stock was traded at ~$6):

Obviously, I think a big portion of our management team's income is tied into RSUs and a significant amount of taxes that you would have to pay out of your own pocket because the management team has not been selling RSUs, unlike some other companies to pay the taxes for it. So that kind of ties up all that -- at least on my part, it ties up all my available cash is to pay 40% taxes on the RSUs. But I think our stock right now is a very, very attractive price.

Given the above facts and hints, I think that management plans to grow rapidly through acquisitions (more about this in a second) and then sell at a higher price, reaping the benefits of both the Change of Control Agreement and the higher equity price for their stock awards.

At least, it is highly likely. But even if the acquisition doesn’t happen, I see the stock easily returning to the $11-12 range and higher when margins normalize and the market sees true levels of Net Income and EBITDA.

By the way, Harborne sold between 22.01.2025 and 07.02.2025, when the stock traded at $11. He stopped as soon as the stock tanked again. This indicates the minimum value for him as a private buyer, and it reinforces my expectation that the stock can achieve this level again.

Why does the opportunity exist at all?

In his letter, Harborne mentioned:

As a long-time investor in the aviation and aerospace industries, I made my investment because I believe the Company has the potential in the long-term to be a best-in-class innovative player in those industries; however, based on my observations since I began investing in the Company, I now firmly believe that the Company is not well positioned to achieve this long-term potential in its current configuration and would be best positioned to do so as a privately-held company.

The premium transaction that I am proposing would allow all of the Company’s shareholders to receive today attractive cash value for this long-term potential without continuing to be subject to the significant operational and financial risks inherent in the Company’s business and the risks inherent in remaining as a shareholder in a small public company with limited access to the capital markets and shares with limited trading liquidity and significant market overhang from shares subject to sale by existing shareholders.

In short, he believes that ISSC has long-term potential but sees three problems. Two of them have already been solved, and one is soon to be solved. I think he saw that and wanted to make an opportunistic buy. But let’s address each of these problems to understand why we have this great opportunity now.

Selling Pressure from Existing Shareholders is Almost Gone

Two years ago, the company's founder and CEO died. Since then, his estate has been selling stocks and has already decreased its stake from ~20% to 5.1%, which has put pressure on the stock price.

However, it seems that they have stopped since they did not sell a single share between 12.01.2025 and 20.02.2025 when the stock jumped to its highest level in 10 years. Even if they still plan to sell, there is not much left.

Enough Internal Cash Flow Generation and Access to Debt Markets is There

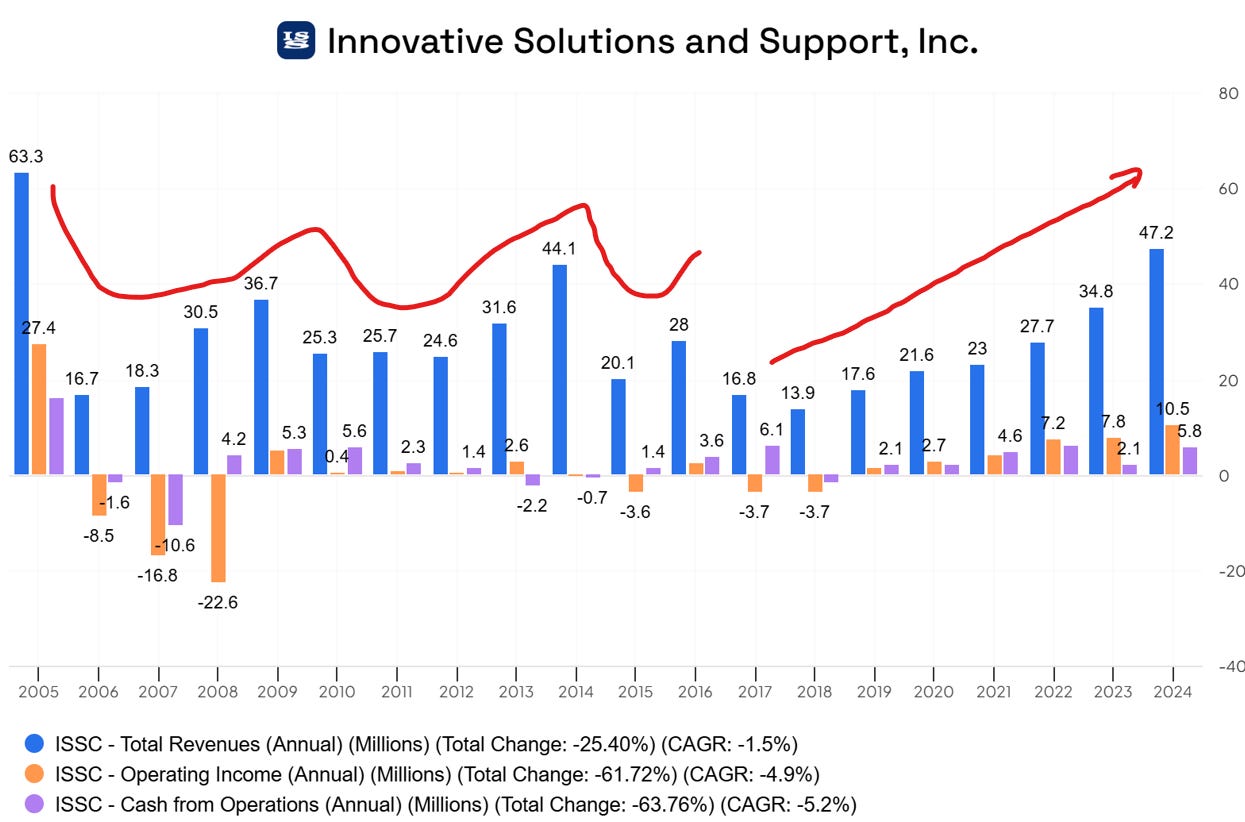

ISSC’s transition from cyclical aftermarket to predictable OEM business remains overlooked by the market. Some investors may be scared by the historical swings in revenues, but it has changed a lot in recent years.

The CEO explained it very well during the investor’s presentation in May 2024:

I'm going to kind of digress a little bit here because I remember a couple of weeks ago, we had a call with 1 of our investors, and he said that, well, your revenue has historically been very cyclic. And how do we know that you're not at top of that curve now? So about 12 years ago, I became president of ISNS and we put a strategy in place to compensate for that cyclicality of the being an aftermarket retrofit business. It was to increase the content in the OEM side to take a lot of that guesswork out of the business. The aftermarket business is always very cyclical because you win 1 big program, you perform on it, and then it goes down until you win another big program to go to catch up. The OEM business is a lot more predictable year after year. You know how many you're going to ship, you know how much revenue you're going to get. So prior to this acquisition, about 60% of our revenue was predictable because of all the OEM programs we've brought in over the last 10 years. And because also the customer service side of the business is also very predictable in terms of how much business you get in a year.

With the acquisition of Honeywell, I think that 60% predictability is more towards 75% now because there is a lot of innovate OEM because we sell parts and spares to channel partners and operators as well as the rest of it goes within the customer service. And so the predictable portion of our business is improved significantly with this acquisition. So this is why we look at all of these things when we look at an acquisition is, does it improve the predictability of our revenue? Does it fall within our within our, portfolio of products, within our customer base, which gives us better visibility and lowers the risk of things not happening the way you expected them.

Given the growing and predictable cash flows in recent years, they were able to start making acquisitions using their internal funds as well as some not-expensive and prudent debt financing.

Recent Growth is Hidden by Temporarily Suppressed Margins

Costs of integration of recently acquired product lines, elevated depreciation and higher inventory costs after acquisitions, expansion of their facilities, and update of the internal IT system create temporary margin pressure. Gross margin is additionally pressured by increased growth in the military segment, which has a similar net margin but a lower gross margin.

In the latest Q1 2025 call, management explained these issues and reiterated that the gross margin will remain a bit lower than historically, while the EBITDA margin will normalize or even improve due to the increased operating leverage:

Our first quarter gross margin was 41.4%, down from 59.3% in the same period last year. As I discussed last quarter, there are several factors that have been impacting our gross margin capture in recent quarters, which continued during the first quarter and will remain a factor in the near term.

…

More specifically, during the first quarter, the impact of the acquired Honeywell military product line volume lower margin was approximately 500 basis points, increased third-party expenses from Honeywell with respect to their transition services was approximately another 200 basis points and higher depreciation from recent acquisitions was roughly a 500-basis point headwind to gross margins.

As it relates to the product mix, generally, military sales carry a lower average gross margin versus commercial contracts. However, there is minimal operating expenses associated with these contracts, so the incremental EBITDA margins are strong. And given the significant potential we see for absolute EBITDA dollar growth in military, we believe this is good for us and work that we will continue to pursue as it advances our focus on improved operating leverage.

In addition to these factors, during the first quarter, we incurred costs to support the ramp-up of recently acquired product lines from Honeywell as well as inefficiencies due to hiring and training additional personnel. Many of these costs were duplicative in nature and will not be a factor as we fully transition the product line into IS&S. Given these factors, we continue to expect our consolidated gross margins will likely trend closer to mid-50% on a normalized basis, which is below historical levels.

Limited investor awareness, thin trading volumes, and volatility are typical of micro-cap stocks. Add to this the history of extreme cyclicality, selling pressures, and bumpy quarterly results, and you have a recipe for temporary mispricing and, therefore, opportunity for us.

Last quarter, ISSC beat expectations by 50% and the stock jumped 40%, this quarter they missed by 60% and the stock fell by 40%.

Solid Business and Financials

From their website:

Innovative Solutions & Support, Inc. (IS&S) is a leading systems integrator that designs and manufactures cost effective NextGen flight navigation systems and precision flight instrumentation equipment for the aerospace industry. The world’s most respected aircraft builders, owners and operators rely on our leading edge avionics technology, superior craftsmanship, and stringent quality standards to significantly enhance reliability, performance and provide superior value.

IS&S is a diversified international supplier to Commercial Transport, Military and Business aviation markets. IS&S products include: Integrated NextGen Avionics Suites, Flight Management Systems, Flat Panel Primary and Flight Navigational Displays, Autothrottles, Engine Instrument Displays, Mission Displays, Integrated Standby Units, advanced Global Positioning Systems (GPS), RNP Navigator and Precision Air Data Instruments.

Some of their customers:

Consistent Organic Growth (10-15%) Supplemented by Strategic Acquisitions

Their first acquisition happened on June 30, 2023, when IS&S acquired certain assets and was granted perpetual license rights to manufacture and sell licensed products related to Honeywell’s inertial, communication, and navigation product lines.

This strategic acquisition allowed them to:

expand and enhance their portfolio

bring some of the expensive third-party production in-house

get access to a huge Honeywell’s customer base for cross-selling of their own products

From Special Call on 13.07.2023:

… having the IP for the radios and the audio systems and the transponders allow us to augment our offerings in the business aviation, where currently we have display systems, but we lacked communication and some of the navigation equipment. It allows us to complement those, where in the past, we would have had to go and partner with other avionics manufacturers and pay significantly higher prices to be able to complete our aftermarket offerings on the business aviation. We can -- now we will have our own products to offer in those markets. And the radios are such that they can be expanded into the military market because their frequency expands into the military frequencies.

… every airplane - 737 classic, 757, 767 - operator in the world is going to become our customer with those inertial reference units. That means we're going to be on the approved vendor list. That means that it opens the door for us to go in there and sell our display upgrades into those platforms.

From Q4 2024 call:

On the heels of our recent Honeywell product line acquisitions, cross-selling synergies have increased as expected. These acquisitions have brought us the opportunity to cross-sell our existing products into new customer relationships acquired in the transactions while also selling new product lines to our legacy customers.

After this acquisition, they guided huge growth in 2024. What is important, they always emphasize that they look only for those acquisitions that either improve or maintain their margin profile:

These product lines have attractive margin profile characteristics that are similar to our current product portfolio, which is an essential element of our strategy. Consequently, once they've been integrated into our operations, we expect the transaction to materially contribute to our revenues and EBITDA. Revenues are expected to grow over 40% while EBITDA is expected to grow roughly 75%.

And they delivered quite well on those promises - revenue grew by 36% and EBITDA - by 50%.

Expansion in Military Segment - Second Honeywell Acquisition

In recent quarters, ISSC saw an increased demand across their military end markets, supported by orders from both the U.S. Department of Defense and allied foreign militaries. Given the current geopolitical situation, I believe this trend will continue.

In order to support this, they made another acquisition from Honeywell in September 2024:

The acquisition we did from Honeywell for the F-16 flight control computer and the mission computer is going to open a lot of doors for us in terms of being at the table with the Lockheed and taking opportunity of other product lines that they are looking to acquire. (Q4 2024 call)

Apart from that, the current administration is encouraging partnerships between traditional defense contractors and innovative tech firms to advance military technologies, including autonomous flight systems, which is one of ISSC’s core competencies:

And given our leadership in cockpit automation, we anticipate a continuation of this trend into 2025. Earlier this year, we announced a new foreign military platform with a major aerospace OEM to supply multifunction displays with an integrated mission computer. We've already begun executing under this contract and realize revenues in 2024. We also recently announced that our ThrustSense Autothrottle system was selected by the U.S. Army to be installed on the C-12 aircraft. This advanced technology will provide full flight envelope protection from takeoff to landing, including go around, enabling pilots to automatically control engine power settings for enhanced safety and efficiency. (Q4 2024 call)

Finally, they are working on becoming a first-tier supplier to DoD (U.S. Department of Defense):

So far, for most part, we've been a second-tier supplier to the DoD. That means that we've always worked through an integrator. Even on some of the OEMs, we've worked through an integrator. We really haven't had any large-sized programs directly with the DoD. And in order to have those kind of contracts and be primed for it, which part of that also applies to the product lines that we bought from Honeywell for the F-16 platform, we've got to be compliant to a lot of these DFARS, the defense acquisition requirements. And so being compliant in terms of account -- what I call a certified government accounting is one of those requirements. Being able to have an IT organization that meets the requirements of the DoD is another one. Having your system in such a way that you can obtain security clearance, you have a means of protecting government documentation. So all of that is required for you to become a Tier 1 supplier to the Department of Defense.

So we're applying for security clearance. We're putting all of that in place. And it gets us to a point we're looking at some of the serious military programs now. (Q4 2024)

we have integrated a modern ERP system, a more robust IT infrastructure and strengthened our security and accounting services to make us compliant with Defense Federal Acquisition Regulation Supplement or DFARS requirements. These are critical investments as we continue to win and bid for larger DoD programs. (Q1 2025)

Tailwinds from Tariffs and On-shoring

ISSC has a 100% U.S.-based vertically integrated production, providing protection from tariffs and benefiting from reshoring trends. They produce everything in-house and the production is highly automated, which increases their operating leverage and allows for higher margins:

We are vertically integrated in our facility in Exton, Pennsylvania. We internally perform all aspects of product development and qualification. We manufacture all products, including all sub assemblies in house. We have an automated surface plant technology laboratory that produces all our electronic circuit cards. We machine our own mechanical parts. We even paint our equipment in house, and our direct cost of labor is less than 5% of our revenue. We achieved this through innovation in product design and automation in the factory. The reduced labor content is what allows us to achieve attractive gross margins as well as enable us to significantly increase our revenue without significant increase in skilled labor. (Special Call May 2023)

We also think it's worth reminding everyone that IS&S manufactures 100% of its products in our Exton facility. We think this is important and puts us in an enviable position as the new administration makes its significant push for reshoring of manufacturing and an America first mentality. (Q1 2025)

It can also open a window for future opportunistic acquisitions:

I mean one of my thoughts is that if our government starts putting tariffs on imports from other countries, a lot of the smaller aviation manufacturers, avionics manufacturers that I know, they outsource their production. They don't have production capabilities. We are kind of very unique in that area that we had manufacturing capabilities in-house for everything. And that's kind of always been the strength of IS&S when it comes to whether there is tariffs, whether there is supply chain issues, our cost of material is small relative to our sales prices because of all the value-added things that we do in-house. So even if material goes up, it doesn't significantly impact our profitability. So that combination and that formula allows us to -- if they stop putting tariffs and a lot of these guys getting the boards made in Southeast Asia, their prices are going to go up. And we may be able to pick them up for a good price and then bring their production in-house and benefit from it. Just an idea that we believe may pay off if we pick the right company. (Q1 2025)

Preparation for More Growth

They are seeing more growth in the future and probably more acquisitions, so they expand their facility to increase their capabilities by threefold:

… we are also continuing the expansion of our Exton, Pennsylvania facility. When completed in mid-2025, we will have doubled our footprint and increased our production capabilities by more than threefold. I watch the progress from my office window every day, and I'm happy to report that the groundwork is complete, the steel structure is up and the completion of the internal and external walls will commence shortly. As a side note, we've been funding this development out of our P&L. Importantly, we are adding this capacity with a capital investment of only $6 million, providing for the opportunity of a very strong return. (Q1 2025)

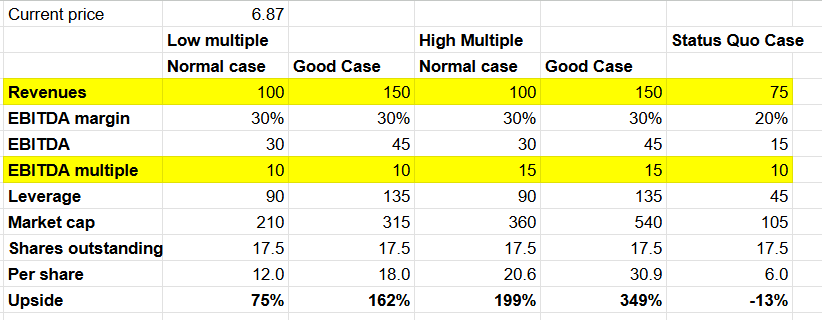

Valuation

There are a few ways to look at valuation.

Firstly, let’s turn to management’s guidance:

As we layer on higher base of revenue within our business, we anticipate improved fixed cost absorption and ultimately, a higher sustained run rate of EBITDA dollars. During 2025, we intend to increase the volume of maintenance, repair and overhaul work we handle at our Exton facility while also increasing the volume of subassemblies that are being manufactured internally. (Q4 2024)

We continue to make significant investments in our growth initiatives, which is impacting our margins in the near term, but will place us in a strong strategic position to take advantage of some of the exciting opportunities in our markets and drive profitable growth in the coming quarters.

… during the first quarter, we made significant investments in support of our most recent acquisition from Honeywell. Much of the spending during the first quarter was made ahead of the expected growth from these platforms, and we also made investments that resulted in some duplicative costs as we train our staff to transition the manufacturing of the products from Honeywell into our Exton facility. The integration is on track, and we are excited by the opportunities from this most recent acquisition.

Looking ahead, we intend to build on the momentum evident within our business and remain on track to deliver both revenue and EBITDA growth of over 30% when compared to fiscal year 2024. (Q1 2025)

Another comment from CEO Askarpour from the Sidoti Micro-Cap Conference (8th May 2024):

A question from the audience about how do you scale up your business? You have very nice growth profile on margins, but how do you what's the pathway to say $100,000,000 in revenue?

So the pathway to $100,000,000 of revenue, we will continue to grow organically by 10% to 15% a year. And again, I like to grow it, including acquisition, by about 40% to 50% a year. And so that's kind of, I think, if we if you're successful on that track within less than 2 years, we should be at $100,000,000 in revenue.

So, management expects between 30% and 50% growth and they expect margins to normalize and probably even improve from higher operating leverage - let’s say a future normalized EBITDA margin will be 30%.

Historically, they’ve been valued at ~15x EBITDA on average. I had a look at some recent M&As and it seems that the average multiple there is also somewhere in the 12-15x range. I will take it as a “normal case” multiple and 10x as a “low case” multiple.

Concerning revenues, I would say that it’s realistic for them to get to somewhere between $100mln and $150mln in the next several years.

At the moment, their leverage is ~1.8x EBITDA, but management mentioned that they see it going up to ~3x, so I took this number.

So, I see the upside from 75% (returning to what we had a few weeks ago) to 3-5x, if it’s not acquired before. I added a Status Quo Case to have a look at what should happen to stay at the same price.

What Harborne was Doing?

A second way is to look at the actions of the largest shareholder Harborne. He wanted to acquire the company at $7.25, which I consider a proxy for margin of safety. And he started selling at ~$11, which corresponds to my lowest level of upside.

Huge Backlog and Revenue Visibility

Yet another way is to look at their current backlog, most of which they got together with the recent acquisition of Honeywell’s military production line.

It’s a significant amount - $81mln, and they said that ~65% is going to be recognized within the next 12 months. This will provide a clear short-term revenue and earnings support of 65% * $81mln = $53mln. This number is already equal to their TTM revenue. It provides another margin of safety that ISSC will be able to meet its targets.

Conclusion

I think that the combination of shareholder/management activity, reduced selling pressure from the estate of the founder, recent strategic acquisitions and growth projects, and temporarily depressed margins creates a great opportunity to buy.

I bought a medium position yesterday.

But don’t expect the ride to be smooth. It was volatile before and it will be volatile in the future. I am ready to buy more if the stock price drops another 25-50% down.

Content I enjoyed recently:

Disclaimer:

I/we own shares of ISSC at the moment of publication.

This article is for educational purposes only. This is not an investment advice. I may buy or sell these securities at any time. Please see the full disclaimer here.

Gold this one, like $GTX report! Thanks Maksim for the work! Hope you Keep doing it. Free or not, I'll be here to suport.

The wording of the contract amendments are interesting. Mr. Askarpour, CEO, seems concerned about being terminated without cause. Think about that.

If you were looking to acquire a company, then wouldn't you want to take ownership of a well run business by keeping the existing management? It's what Buffett does. Management comes first.

If Mr. Askarpour is concerned about being terminated post acquisition, does that suggest that there is tension between the majority shareholder and the board?

Why would that be?

An alternative interpretation is that Mr. Askarpour is putting his own personal interests before those of the company and its shareholders. He should want what is best for the business and if that means a change of ownership, so be it. But he seems concerned that the new owner would oust him.

The levels of stock based comp (RSU and PSU) relative to net income, and consequential shareholder dilution, also suggests that management is not motivated by what is best for shareholders.

Harborne's letter states, "I now firmly believe that the Company is not well positioned to achieve this long-term potential in its current configuration... [and if he acquired the business, shareholders would not be] subject to the significant operational and financial risks inherent in the Company’s business."

To me that sounds like he has no faith in the existing management being able to deliver on the company's potential.

Revenue has increased over the past few years, but at the expense of margins.

The CEO talks a good game, but there is tension here for sure. Either Harborne is right or the CEO is right, but they can't both be right. Since Harborne is putting his own money behind his belief, I am more inclined to believe his position than I am to believe a CEO who is self interested and tries to enrich himself with PSUs and RSUs and changes to his contract of employment.

I may be wrong, but something doesn't smell right here. I like to see harmony in a business between owners and management - not conflict. For me this isn't investing, it is speculating in the hope of a favourable outcome. Just my opinion - I may be entirely wrong, but I'll pass on this.